Profile

Profile Settings

Settings Refer your friends

Refer your friends Sign out

Sign out

A Voucher is a document which acts as proof of a business transaction. It is not important how the voucher looks; all that counts is that it serves as proof of a transaction. When you enter a transaction, you’re also confirming the proof of that transaction. A voucher aids in the documentation of expenses or liabilities, as well as their payment.

Voucher

A voucher is an accounting record which shows the flow of resources inside or outside the business, whether they be commodities, assets, or money. It approves receipts and payments and displays the ledger account where the transactions are recorded. In general, invoices, cash memos, receipts, receipt counterfoils, written requisition slips, meeting resolutions, and pay-in-slips. In the corporate world, purchase invoices, debit notes, and credit notes are all crucial documents that are used as vouchers. Furthermore, the voucher has no set format, which is why it varies from one organisation to the next.

In accounting, a voucher is a document that the accounts payable department uses to approve payments. It can also be referred to as a liability memorandum for any company. An accounting voucher can be thought of as a written backup document for payments made to suppliers or creditors in any organisation for work done with the party.

Classification of Vouchers

Voucher is classified on the basis of :

- Recording of transactions

- Source

Classification of Voucher on the basis of Recording of transactions

Voucher is classified in three types which are as follows:

- Transaction Voucher

- Compound Voucher

- Complex voucher

Transaction Voucher

Simple transactions have only one debit and credit, and the vouchers created for these transactions are called Transaction vouchers.

Compound Voucher

Compound transactions are those that have many debits or credits but only one debit or credit. And compound vouchers are those that are created for compound transactions. A compound voucher is a voucher that the company creates for two different sorts of transactions. The first category involves transactions in which multiple accounts are debited but only one account is credited. The second category involves transactions in which multiple accounts are credited but only one account is debited.

There are two types of compound voucher which are given as:

- Debit Voucher

- Credit Voucher

Complex Voucher

Complex transactions are defined as transactions with many debits and credits, and the voucher created for them is referred to as a complex voucher or journal voucher.

Classification of Voucher On the basis of source

Voucher is classified in three types which are as follows:

- Primary Voucher

- Collateral Voucher

Primary Voucher

A primary voucher is a written documentary proof that is still in its original form. Purchase invoices, cash receipt counterfoils, and other documents may be included.

Collateral Voucher

Collateral vouchers are used when the original written documented proof is missing but copies are available. Copies of such documents are given for auditing purposes in such circumstances. One common example of collateral vouchers is photocopies of demand draughts.

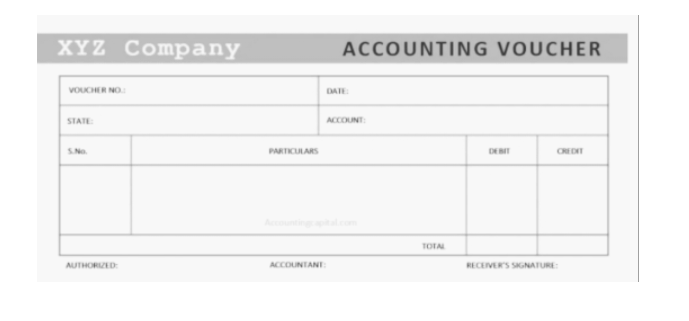

Format and Elements of Vouchers

Because there is no standard structure for an accounting voucher, several types of accounting vouchers exist based on the nature, requirements, and convenience of the business. Individual vouchers are created for separate items of expense, and the business utilises different colour papers and fonts to distinguish them.

An accounting voucher must include the following fundamental characteristics in order to be useful:

It should be printed on high-quality paper.

On the top of the voucher, the name of the firm/company/business/enterprise should be printed.

The date of the transaction should be written on the entire voucher.

All vouchers should be created in a sequential order based on the date the transactions were completed;

Name of the account to be debited or credited must be mentioned on the voucher.

The data and information on a voucher basically include:

- The voucher numbers.

- Date as well as types of accounting vouchers.

- Column for Credit and debit.

- Particular column which involves a brief explanation of the record of transaction.

- Identification Number of suppliers.

- The amount payable in words as well as in figures.

- Due date for the payment.

- Name of account under which liability is generated.

- Terms and conditions for the discount and other schemes.

- Signature of Receiver.

Conclusion

A voucher is an accounting record which shows the flow of resources inside or outside the business, whether they be commodities, assets, or money. Voucher is classified, on the basis of transaction, in three types which are Transaction Voucher, Compound Voucher and Complex voucher. Voucher is classified, on the basis of source, in two types which are Primary Voucher and Collateral Voucher. A compound voucher is a voucher that the company creates for two different sorts of transactions. There are two types of compound voucher which are given as Debit Voucher and Credit Voucher.