Profile

Profile Settings

Settings Refer your friends

Refer your friends Sign out

Sign out

Production is the interaction by which sources of information are changed into “yield.” Production is done by makers or firms. A firm uses various elements of creation (inputs) like land, work, machines, unrefined components, and so forth to deliver a yield. This outcome can be consumed by customers or used by other businesses to generate additional revenue.

Notwithstanding, to procure inputs, a firm needs to pay for them. This is known as the “cost of production.” Whenever enough has been delivered, the firm sells it and makes an income. The distinction between income and cost is known as the company’s benefit.

Production Function

- It is a relationship between inputs used, and the output produced by the firm

- It gives an idea of the maximum quantity of output that can be produced for various quantities of inputs used

- It is defined for a given technology. The output will be attained at maximum levels for a different increase in input combinations when technology improves. The maximum levels of output attainable for different input combinations increase. We then have a new production function

Production Time Concepts

- Short Run: In the short run, at least one of the factors, either labour or capital, cannot be varied, and therefore, remains fixed. Therefore, to vary the output level, the firm can vary only the other factor. The factor that remains fixed is called the “fixed factor,” whereas the other factor that the firm can vary is called the “variable factor”

- In the long run, all factors of production can be varied due to the long time frame being considered. There is no fixed factor in this concept

Other important terms related to production:

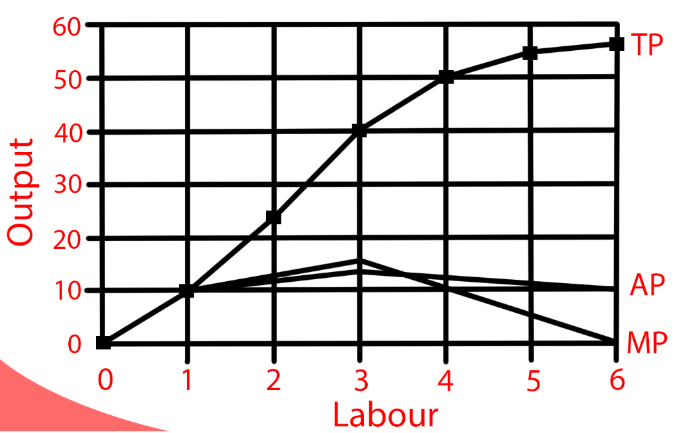

- Total Product (TP): It is a relationship between variable input and variable output. product is the output received at a particular level of the variable input, keeping all other factors constant

- Average product (AP): It is defined as the output per unit of the variable input

- The marginal product of an input (MP): It is defined as the change in output per unit of change in the input when all other inputs are held constant. The total product at each level of an input is the sum of the marginal products of every previous unit of that input

- Law of variable proportions: It is defined as the marginal product of a variable factor input that initially rises with its input level, but after reaching a certain level of employment, it starts falling

Fig: Curve (TP, AP and MP)

Beyond a certain point, the production process becomes too crowded with the variable input and further effectiveness can only be attained by enhancing the fixed input. However, this is a short-run concept, as in the long run, all the factors are variable.

Returns to Scale

- It is the quantitative change in a firm’s results caused by a proportionate expansion in all data sources

- When a proportional increase in all inputs results in an increase in output by the same proportion, the production function shows a constant return to scale (CRS)

- When a proportional increase in all inputs results in an increase in output by a larger proportion, the production function is said to display “Increasing Returns to Scale” (IRS)

- Diminishing Returns to Scale (DRS) holds when a corresponding expansion in all data sources brings about an increment in yield to a more modest extent

Costs

Cost is the monetary value of all the expenditures for raw materials, equipment, labour, etc., required to produce goods and services. For every level of output, the firm chooses the lowest-cost input combination to achieve price competitiveness and maximize profit.

In this manner, the term “expense work” reflects the minimal expense of creating each degree of the result, given the costs of creation and innovation.

- Complete Fixed Cost: In the short run, a portion of the variables of creation can’t differ, and in this way, they stay fixed. The expense that a firm incurs to utilize fixed information sources is known as the “complete fixed expense”

- In the short run, the firm can only change a few input variables to achieve any desired level of result. Similarly, the expense that a firm incurs to utilize these various data sources is known as the absolute factor cost (TVC)

- The total cost per unit of output is defined as the short-run average cost. At zero output, the short-run average cost is undefined

- Short-run marginal cost: it is defined as the change in total cost per unit of change in output

Average Variable Cost: It is defined as the total variable cost per unit of output in short-term production. If the price of a good is higher than the average variable cost of the good, the firm is covering all the variable costs and a percentage of the fixed costs. In this case, firms continue production

Conclusion

This chapter defines concepts of production such as production function, short period, long period, fixed factors, variable factors, and concepts such as total product, average product, and marginal product, as well as their interrelationships. The law of variable proportion in concepts of production and its phases is explored using reasoning.