Profile

Profile Settings

Settings Refer your friends

Refer your friends Sign out

Sign out

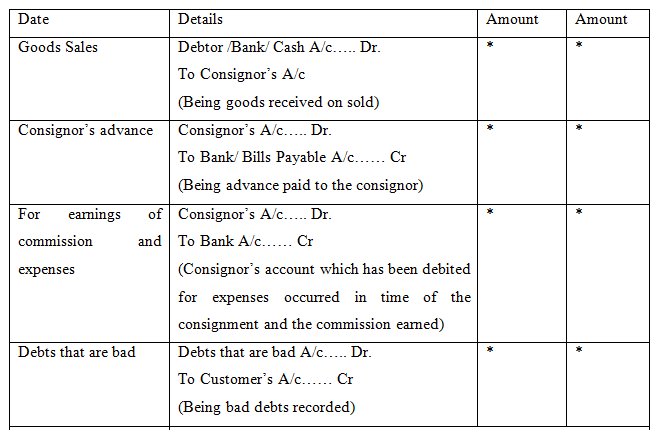

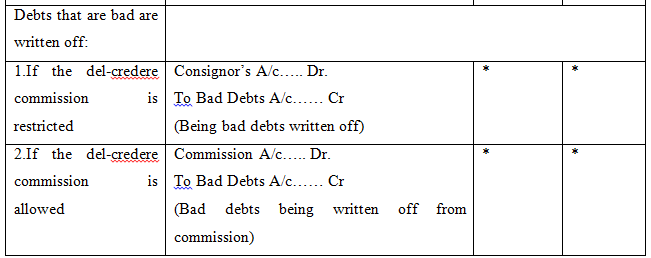

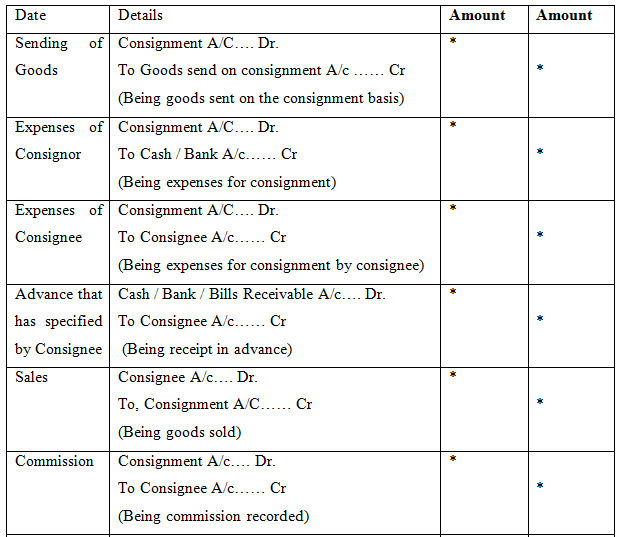

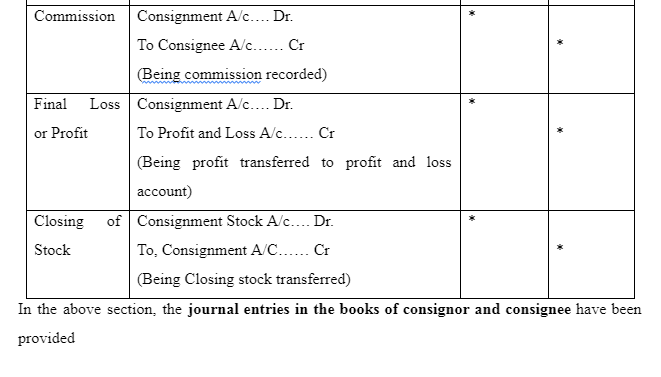

The article is written on the core accountancy topic of the consignment. Under this main topic, the meaning of consignee and some other subtopics including consignment accounting entries in the books of the consignee, journal entries in the books of the consignee, journal entries in the books of consignor and consignee will be discussed