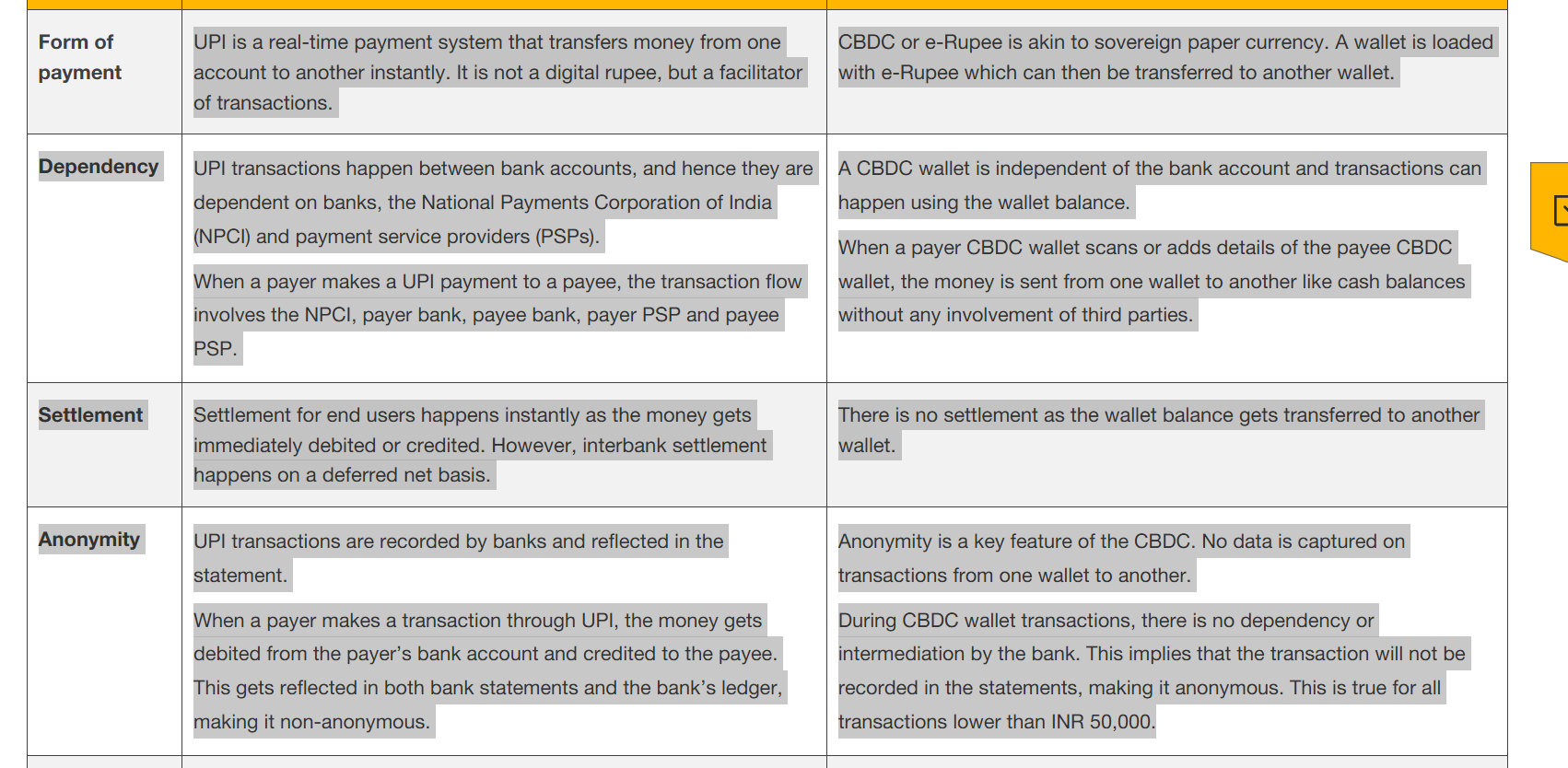

(d) is not correct: Unlike UPI, which moves commercial bank money, the e-Rupee is a direct liability of the central bank (RBI), carrying zero credit or settlement risk. So the liability for Digital Rupee lies with the RBI, not with users and their banks. Option (d) wrongly equates the liability structure of both.

(a) is correct: UPI is a real-time payment system; Digital Rupee is sovereign currency like paper money.

(b) is correct: In UPI, the amount is debited and credited instantly as a ledger entry, but actual fund transfer happens during the bank settlement cycle. In CBDC, there is an exchange of tokens in real time — as good as handing over a physical note — eliminating the need for a settlement process.

(c) is correct: RBI has designed small-value Digital Rupee transactions to offer anonymity similar to cash — it won't appear in your bank statement, unlike UPI transactions.

Source:

https://www.pwc.in/research-and-insights-hub/future-of-digital-currency-in-india.html

Profile

Profile Settings

Settings Refer your friends

Refer your friends Sign out

Sign out